Building your first home? The construction process can be a hefty but exciting one. And while it’s tempting to skip straight to floor plans and fixtures of your dream home, there’s one key foundation you need to lock in first: finance. But what is a construction loan, and how does it work? This special type of finance operates a little differently from a regular mortgage for an established home. And because it’s for building rather than buying a house, it’s made specifically to protect you and the lender during the construction process.

In this guide, we walk you through construction loans, how you make payments during the build, and what lenders are looking for. You could be stepping into your dream home sooner than you think.

What is a construction loan? The basics

Before we get into the application process, let’s answer the commonly asked questions: what is a construction loan, and how does it differ from a regular mortgage? Simply put, a construction loan helps finance building a house or undertaking major structural renovations. Compared to a regular home loan, where you’d get the full loan amount upfront to pay for a ready-built home, a construction loan is released in stages throughout the build.

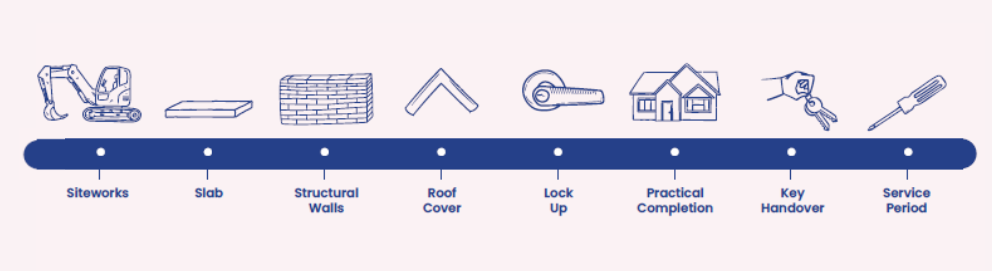

These stages usually align with key phases of your home build, including:

- Paying the deposit

- Laying the slab

- Roofing and tiling

- Internal finishes

- Lock-up

- Completion

Known as ‘progress payments’, they’re a way to protect both you and your lender by ensuring that funds are released to the builder only as construction moves forward.

Thanks to this structure, construction loans often start with interest-only repayments, so you only pay interest on the amount drawn down at each stage. Once your home is complete, the loan typically switches to a regular principal and interest loan.

How does a construction loan work?

Curious about getting a loan to build a house? At Easystart, our new home consultants work alongside a dedicated Westgate Finance broker to support your building dreams. These brokers specialise in construction loans for Easystart buyers, so you know you’re in safe hands.

Here’s what the construction loan approval process looks like, step by step.

Step 1: Choose your land and home design

Start shopping around for a block of land and home design that suits your lifestyle and budget. If you’re building with us, once you’ve chosen your site and design, we’ll give you a building contract. You’ll use this for your loan application, as it tells the lender how much your build will cost and when the progress payments are required.

Step 2: Get pre-approval

Your Westgate Finance broker can help you understand what is needed for a construction loan, your borrowing power, and any available grants (including the First Home Owner’s Grant). From there, they’ll give you a conditional approval amount with a potential lender, so you know how much money you have to complete your new build. Once your home design and building contract are in place, you’re ready to apply for a loan to build a house. Lenders will assess your financial situation, just like with a regular home loan, but they’ll also look closely at your builder and contract.

Step 3: Loan approval and settlement

Congrats, your loan is approved! Now, your lender will settle the loan and start releasing payments directly to your builder at each stage of construction, as determined in the contract.

Step 4: Move in and maintain your loan payments

While your home’s being built, you’ll make interest-only payments. But once it’s finished, your standard repayments will begin. It’s time to enjoy your new home.

Can I get a loan to build a house if I already own one?

Sometimes, getting a loan to buy land and build a house can be tricky if you’re still paying a mortgage on your existing home. Enter the bridging loan. This finance option offers short-term funding that helps cover the gap between buying land, building and selling your existing home.

A bridging loan lets you access the equity in your current property to fund your new build. However, it comes with extra considerations, such as shorter loan terms, higher interest rates, and the need to service two loans simultaneously.

Curious about the best type of loan to build a house? Our finance team can help. We’ll assess your situation and weigh up options such as bridging loans, equity loans and other finance options to find the right fit.

Building your finance foundation

Whether you’re just starting out and planning to build a house in Perth or already own your home and are looking for a fresh start, a construction loan could be the answer. By breaking it down into steps, including pre-approval and progress payments, you’ll feel more in control and prepared for the journey. Contact Easystart Homes today to start the process.

All finance services provided by Westgate Financial Services, ACL. 410232.